Cyber winds ༄༄

Disruption of decade-long macro-economic trends is never easy, let alone when you’re trying to disrupt the tech market yourself. It may feel like shooting a moving target and it is difficult to be prepared for it.

This is why I felt the need to start writing about infrastructure software at this time. Talking to founders, companies and investors, a common topic throughout last year was the market sentiment, most resilient tech segments, etc. The goal of this monthly newsletter is precisely to share some of those insights and contribute to better navigating these turbulent times. All with a focus on infrastructure software, namely DevOps, ML/Data and Cybersecurity. We make the road by walking, so let’s start.

As of end January 2023, it’s the first time since early 2022 that public market multiples across infrastructure software seem to be consistently breaking the trend of decline, even before the earning announcements of 2022. Still, average and median Revenue multiples sit at 8.3x and 6.8x, more than 50% below the start of 2022.

Only now we are starting to see the depth of the macro-economic slow-down that started in early 2022, with Revenue growth at 30% CAGR across public infrastructure software companies, pretty much on the upper range of the growth of major cloud vendors, whose growth decelerated to 20–30% CAGR in end 2022 (versus 40–50% CAGR in early 2022, only surpassed by Cloudflare).

On the private funding market, most founders in ‘fair performance’ companies are still facing serious difficulties in raising or already committed to skip fundraising (preferring internal bridge rounds). Only top performing growth stage scale-ups or early stage start-ups with huge potential seem to weather the storm.

On the venture side, most notable rounds that took place in January:

Netskope secured 401M$ in funding via convertible note, pushing out valuation discussions

QuickNode raised 60M$ Series B within Web3 app dev platforms, in a tough context for crypto and web3

Egerie raised 30M€ from existing investors Ace as well as new investors Open CNP or TIIN, to accelerate in Cyber Risk Management — congrats to the team!

AtomicJar raised 27M$ Series B from Insight and Boldstart to focus on automating application testing across any environment, underpinned by the traction of the open-source Testcontainers project — congrats Sergei and team!

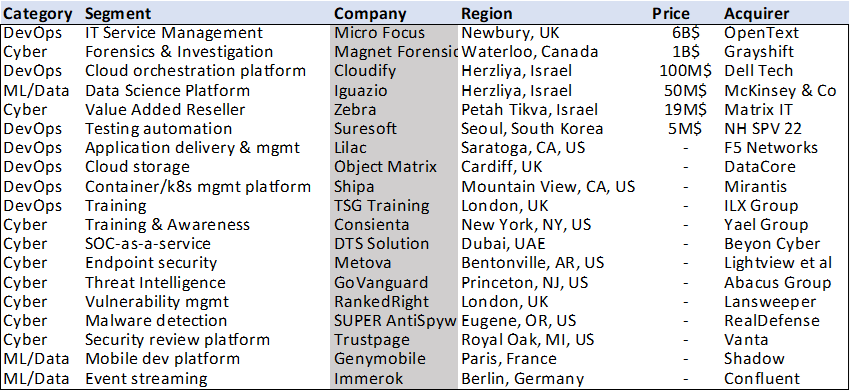

On the M&A side, expected signs of market consolidation are starting to show, with consolidators now active and scale-ups valuing the opportunity to join forces under the restrictive funding environment and slower moving commercial traction. Most notable deals included:

Micro Focus joined forces with OpenText in a 6B$ deal (2.3x Rev and 6.7x adjusted EBITDA multiples) to consolidate services across Cyber, DevOps and ML/Data; the companies then announced a 8% workforce reduction

Magnet Forensics and Grayshift combined after a 1.4B$ buy-out to create a larger player in Cyber Forensics & Investigation

Cloudify was acquired by Dell for up to 100M$, for its stance as Infrastructure-as-code (IaaC) platform — congrats Ariel and team!

Iguazio was acquired by McKinsey, in an unusual deal of a Data Science platform being acquired by a tier-1 management consultancy — congrats Asaf Somekh and team!

Immerok was acquired by Confluent, having been built by maintainers of Apache Flink and focused on event streaming infrastructure — congrats!

The winds keep on blowing. Looking forward to next month.

Thanks for this post. It would be great if you could post tables instead of images - it would be easier to search for particular orgs and export the data for further analysis.